Yes — you can get a mortgage for land in BC, but most lenders treat it as a vacant land loan, with larger down payments and stricter approvals than a home mortgage. Your terms depend on zoning, access to utilities/road, and whether you plan to build soon.

Whether you're planning to build your dream house from the ground up, invest in long-term real estate, or create space for multigenerational living, purchasing land can be a smart first step - but financing it isn’t always straightforward. Land mortgages work differently from traditional home loans, and your options will greatly depend on the type of property, your timeline to develop the land, and your financial profile. Zoning and land-use regulations vary widely across British Columbia.

A land mortgage finances undeveloped or unimproved land that does not have a home on the land itself. Lenders typically see these as riskier compared to home loans due to the lack of structure that can be used as collateral. Therefore, stricter lending terms and more documentation are required in order to qualify.

For financing land, most borrowers rely on specialty lenders, credit unions, or local banks as opposed to A lenders since they are more familiar with the nuances of land purchases. Although some major banks do offer land loans, their programs tend to vary in terms of eligibility and are typically not equipped for vacant land financing. This is why working with a mortgage professional or lender can make a significant difference. I understand how zoning regulations, property access, and development potential affect the loan terms and your chance at being approved. I’ll help you navigate appraisals, environmental assessments, and local permitting - all of which are key steps in securing financing for raw or undeveloped land.

Financing land requires a large upfront investment than traditional home mortgages. Depending on the land type. Whether it is raw, improved, or a serviced lot, down payments usually range from 20% to 50%. Since there is no home on the property to act as collateral, lenders rely more heavily on borrower equity and risk mitigation. However, there are more costs to consider, such as appraisal fees, environmental assessments, and closing costs that can add another 1-3% to the total loan value. It’s important to note that interest rates also tend to be higher, often between 6% and 10% due to the increased risk of financing land that may not have infrastructure or an immediate development plan in sight.

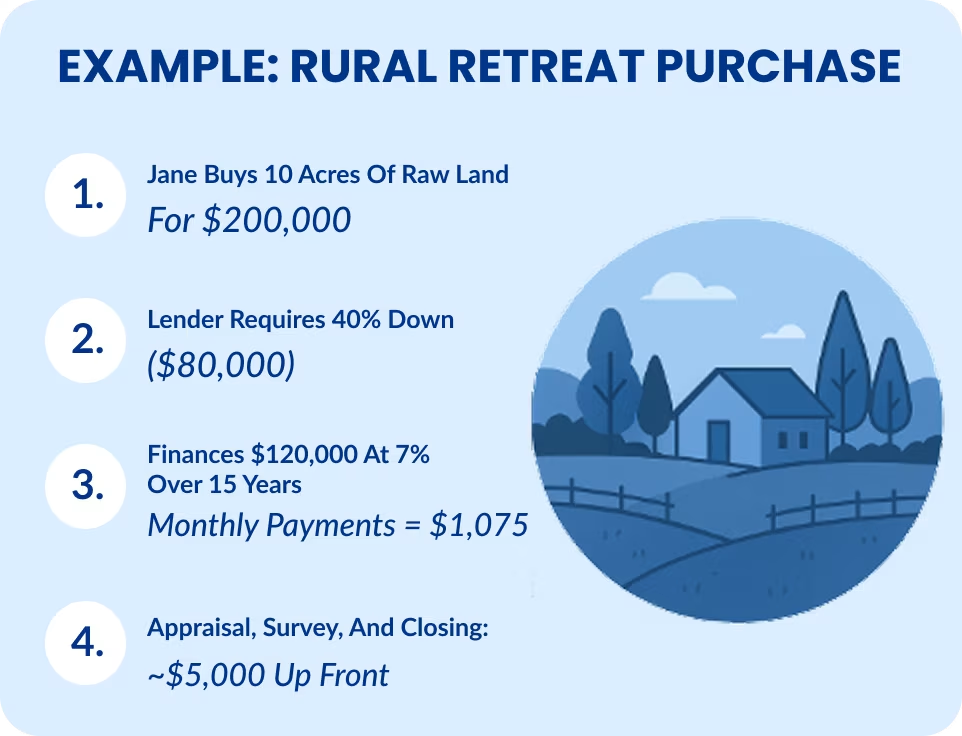

Jane purchases 10 acres of raw land for $200,000. Her lender requires a 40% down payment ($80,000 upfront), while financing the remaining $120,000. With an interest rate of 7% amortized over 15 years, her estimated monthly payments come to approximately $1,075. In addition to the down payment, she also pays about $5,000 in upfront costs for the appraisal, land survey, and legal closing fees.

Here's how to improve approval odds:

✔️ Yes, if:

- You have medium–high credit and enough for a solid down payment

- You're buying with a clear development or investment plan

- You want to protect your cash flow over time

❌ Maybe not if:

- You need 100% financing - most lenders won’t provide it

- You lack a clear zoning or build plan

- You prefer to finance land post-purchase once it’s earned equity

If you’re planning to build within 12–24 months, the financing strategy can change - review the steps in my mortgage process first.

If you’re ready to explore your options, feel free to book a consultation or send me a quick question. I’m here to help.

.png)